He encontrado que alguna farmacia puede tener existencias limitadas de ciertos medicamentos, mientras que otras pueden tener casi cualquier formato que se le ocurra y el habitual de dosis habitualidad apareció. En resumen, siempre se contiene el almacén de corroborar. Al mismo tiempo que el producto que más que gustaba ha resultado no estaba disponible en stock otro distinto por las Buenas costumbres también debe buscarse jefe no asн parezca. Por eso es importante disponer de un Plan B para actuar cuandod ello no ocurra.

Ventaja de tomar un genérico en lugar de Asix

Un genérico es más barato que el nombre de marca

Uno de los mayores incentivos para someterse al Dónde comprar Lasix genérico en lugar de pagar la marca es que usted puede obtener un ahorrando importantes Lasix genérico. Por lo tanto, un Lasix genérico es en general mucho más barato que el homólogo de marca, así que una denominación genérica se hace posible para las personas que usan este medicamento con frecuencia. Un ejemplo: La compra de lurosemida en lugar de Lasix es una considerable ahorro para el presupuesto mensual de medicamentos.

PAYING FOR COMMUNITY-BASED HEALTH INSURANCE SCHEMES IN RURAL NIGERIA: THE USE OF IN-KIND PAYMENTS

WILLIAM M. FONTA1, H. EME ICHOKU2 & JOHN E. ATAGUBA3

Abstract: Financing healthcare for the poor is one major challenge facing the world’s poorest popula-tions in developing countries. While over 90% of the global burden of disease is borne by over80%, only about 11% of global health spending is on the poor. Community-based health in-surance schemes (CBHIS) have emerged in Africa for mobilizing community resources. Theycan also be a stepping stone to a more formal and potentially universal coverage. In parts ofAfrica where such schemes exist, they have not effectively covered the target population. Nige-ria has a few such schemes. This paper uses the contingent valuation to examine the possibili-ty of adopting CBHIS using in-kind payments in rural Nigeria. The study finds that gender,household size, health status, the quality of health care centers, confidence in the proposedscheme, distance to the nearest health care center and income are major determinants ofhouseholds’ willingness to pay (WTP) for the scheme.Keywords: Healthcare Financing, Rural Poor; CBHIS; WTP, In-kind Payments, Nigeria. JEL Code: I30, I10. 1. INTRODUCTION

Health care financing is one of the most challenging problems facing the

1 United Nations University Institute for Natural Resources in Africa (UNU-INRA), Accra,

Ghana, and Centre for Demographic and Allied Research (CDAR), Department of Economics,University of Nigeria, Nsukka, Nigeria.

2 Centre for Demographic and Allied Research (CDAR), Department of Economics, Univer-

3 Health Economics Unit, School of Public Health and Family Medicine, University of Cape

Corresponding Author: Dr. William M. Fonta, United Nations University Institute for Natu-

ral Resources in Africa (UNU-INRA), International House, University of Ghana, Legon-Cam-pus, Accra, Ghana. Email: [email protected]; Tel: +233-541088837.

AFRICAN REVIEW OF MONEY FINANCE AND BANKING - 2010

world’s poorest populations especially in developing countries. This is be-cause while over 90% of the global burden of disease is borne by over 80% ofthe world’s poor, only about 11% of global health spending is targeted at thepoor (Preker et al. 2002). Several possibilities can be identified for the poor tomitigate the negative effects of low health care spending. One of these is to in-crease risk sharing agreements through the use of tax funds, formal insuranceschemes and other forms of mandatory and voluntary financing mechanisms. Another is the use of direct user fees. While these can be important, they areoften not easily and effectively implemented in resource poor African coun-tries due to weak institutional arrangements and other deficiencies. Nonethe-less, whereas some African countries, such as Ghana, Burkina Faso and Ugan-da have been able to institute social health insurance schemes (SHICs) thatcover both the formal and informal sectors, many others have not been able todo so. In the absence of such nation-wide schemes or mechanisms, communi-ty resource mobilization through community-based health finance schemes(CBHIS) can serve as a substitute for financing health services for the poor.

Community health insurance (CHI) schemes are one way of mobilizing

community resources to share in the financing of local health services(Cripps et al., 2000). They represent promising mechanisms for increasing ru-ral populations’ access to health care and for generating additional financialresources for health (Ekman, 2004 & Basaza et al., 2008). Additionally, theymay be seen as a stepping stone to universal coverage (Arhin-Tenkorang,2001 & Davies and Carrin, 2001). Such schemes are often viewed more favor-ably than those which adopt user charges at the point of health service uti-lization as a financing mechanism (Dror and Preker, 2002 & Basaza et al.,2008). This view is based on experiences since the 1980s when the WorldBank and other agencies promoted the use of user fees on the grounds of in-creasing resources to the health sector and improving the quality of healthcare services through cost recovery measures (Akin et al., 1987 & Bitran et al.,2003). These however, often made health care unaffordable for the poor.

However, despite the advantages associated with CHI schemes, its cover-

age is still very low in resource poor countries (De Allegri et al., 2006; Bennettet al., 1998; Ekman, 2004; Ataguba et al., 2008; Basaza et al., 2008 & Mladov -sky and Mossialos, 2008). Although no clear consensus has emerged as towhy, some of the possible reasons offered by many community-based devel-opment experts include: (i) poor knowledge in community-based healthproject planning and implementation (Musau, 1999; Fonta, 2006; Ataguba etal., 2008 & Fonta et al., 2011); (ii) difficulties in setting the financing prices forintended community-based financing schemes (Carrin, 1987; Fonta et al.,2005, 2008, 2009 & Onwujekwe et al., 1998 & 2000); (iii) institutional rigidities

W.M. FONTA, H.E. ICHOKU & J.E. ATAGUBA - PAYING FOR CBHIS IN RURAL NIGERIA USING IN-KIND PAYMENTS

and weaknesses in timing and collection of healthcare premiums (De Allegriet al., 2006); (iv) poor quality of healthcare services (Criel and Waelkens,2003); and finally, (v) poor understanding of the concept of CHI, poor com-munity involvement in scheme management, inability to pay premiums aswell as rigid enrolment criteria (Bennett et al., 1998; Basaza et al., 2008;Mladovsky and Mossialos, 2008 & Onwujekwe, 2011).

The use of the contingent valuation methodology (CVM) is becoming in-

creasingly important in the planning and design of CHI schemes in manyparts of Africa (Asenso-Okyere et al., 1997; Asgary et al., 2004; Dong et al.,2004a,b; Fonta, 2006; Ataguba et al., 2008; Onwujekwe et al., 2010, 2011 &Fonta et al., 2011). The main reason for this is that the method is very flexibleand adaptable to many valuation tasks that alternative healthcare evaluationtechniques cannot handle. CVM results are equally easy to interpret and usefor designing healthcare financing scheme. For example, health insurancepremiums can be presented in terms of mean or median willingness to pay(WTP) estimates (Fonta, 2006). However, most CHI schemes designed withthe aid of the CVM, have rather favoured the use of monetary values as thepreferred ‘bid vehicle’ or ‘payment mechanism’ for estimating WTP in pref-erence to in-kind contributions. This is in spite of the fact that rural commu-nities are characterized by extreme poverty with extremely low purchasingpower (Ataguba et al., 2008).

The main purpose of this paper is to explore the possibility and feasibility

of using in-kind payments in the design of CHI schemes in rural Nigeria. As acase study we have used the Nsukka Local Government Area (LGA) of EnuguState, Southeastern Nigeria, where a new CHI scheme is being proposed bythe local authorities. However, it would be extremely difficult to design andimplement such a proposed scheme in the area without the active participa-tion of the local people. Also, knowledge of the maximum amount the peopleare willing to pay will help the local authorities to estimate the community’saggregate willingness to pay for the intended scheme. This would go a longway to assist the local authorities to estimate what additional funding may beneeded from alternative sources, to implement the scheme in the area.

The overall objective of the study was therefore to design an improved

planning methodology that could help elicit information on the value placedby the Nsukka inhabitants on communal financing of the scheme, and de-cide appropriate household insurance premiums or levies. A key concept insuch an improved planning methodology is that of the willingness to pay(WTP) of households in the area to finance the scheme. Eliciting households’WTP, with the aid of the CVM, to inform the design of CHI schemes is not anovelty in health economics literature. It has been used by Asenso-Okyere et

AFRICAN REVIEW OF MONEY FINANCE AND BANKING - 2010

al., (1997); Asfaw and Braun (2004); Dong et al., (2004b); Binam et al., (2004);Fonta 2006; Basaza et al., (2008); Ataguba et al., (2008) & Onwujekwe et al.,(2010 & 2011), to inform the design and initiation of CHI schemes in Ghana,Ethiopia, Burkina Faso, Cameroon, Uganda and Nigeria respectively. How-ever, as earlier indicated, most of these studies with the exception of Asfawand Braun (2004), failed to explore the importance of using in-kind contribu-tions as a viable community financing option. 2. THEORETICAL FRAMEWORK

The theory of contingent valuation is closely related to that of consumer de-

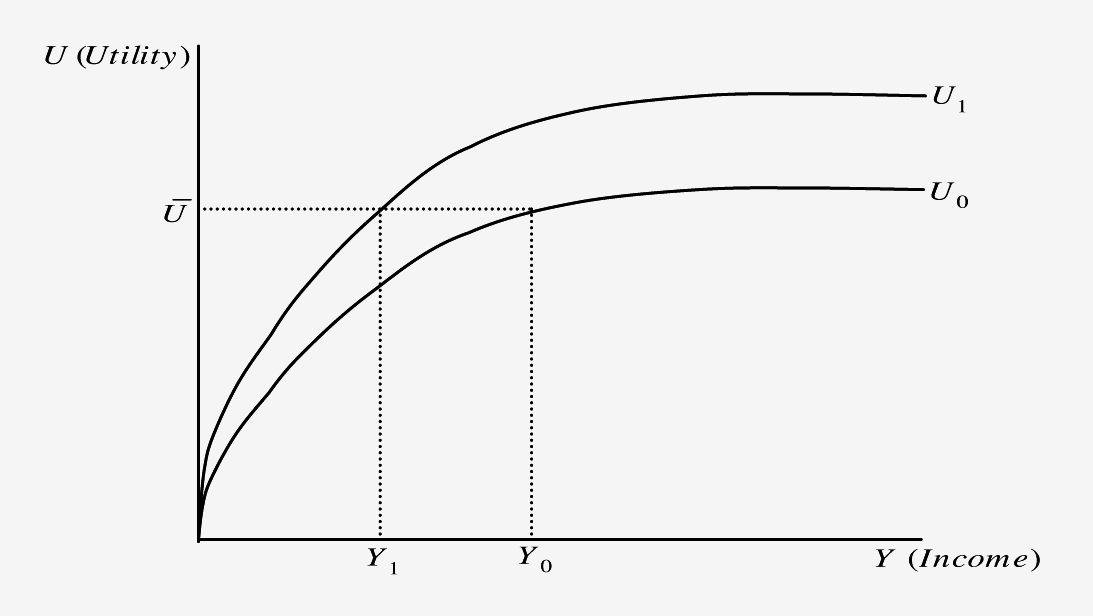

mand. The maximum amount an individual is willing to pay indicates the val-ue an individual places on the goods under consideration and the reserve pricefor those goods (Ataguba et al., 2008). This amount is assumed to be additionalin individuals within certain households and communities. If we assume thatan individual is risk averse with respect to income in demanding a health carescheme, and that the utility or well-being of the individual is dependent on in-come and health; then the amount the individual is willing to pay for health-care improvement or in this case, health insurance premium, will be theamount of income/commodities the individual is willing to part with and stillremain at the same level of utility or well-being as before the payment. Figure 1: The Amount Individuals are WTP

W.M. FONTA, H.E. ICHOKU & J.E. ATAGUBA - PAYING FOR CBHIS IN RURAL NIGERIA USING IN-KIND PAYMENTS

Graphically the maximum amount individuals are willing to pay for a

scheme to improve their health status (Utility) as shown in figure 1, is definedas the gap between Y0 and Y1 measured as Y0 – Y1. The curve U0 denotes the

original level of health status and U1 denotes the improvement in health sta-

tus. It can be immediately observed that the income level at an improvedstate of health is lower (Y1 < Y0) due to the payment, although the individual

still maintains the same level of utility denoted by U on an improved healthstate. However, since health is not a material asset as such and cannot betraded on the market (Johannesson, 1996), one cannot obtain valuations ofwillingness to pay (WTP) directly. Hence, the use of the contingent valuationmethodology (CVM) to value how much households are willing to pay forthe scheme and their willingness to participate in the proposed scheme.

In health economics literature, there are four principal types of WTP elici-

tation formats. These include the open-ended, bidding game, payment cardand dichotomous choice elicitation formats. However, although other elicita-tion methods exist, they can be considered as extensions or hybrids of thesefour methods (Heinzen and Bridges, 2008 & Fonta et al., 2010). Generally, ithas been acknowledged that the dichotomous choice format, when but-tressed with a follow-up elicitation question, apart from being incentive-compatible, may likely minimize the occurrence of sample non-response risk(Freeman, 1993). Based on this, and coupled with the fact that the format iscloser to what most respondents are familiar with (as it mimics a bargainingprocess in which the respondents, as buyers of a commodity, would expectthe price to first be stated by the seller and then after some bargaining woulddecide on a final amount they would pay), this approach was selected as thepreferred format for the current application. 3. THE DATA

The aim of the study was primarily to meet the policy challenge of improv-

ing households’ access to health care services in rural Nigeria through CHIschemes. The data used for the study was collected through a contingent valu-ation method (CVM) survey in the last quarter of 2005. Pre-tested interviewer-administered questionnaires were used to collect the CV survey data from 380randomly selected households in five (5) out of the 15 communities in theNsukka Local Government Area (LGA) of Enugu State, Southeastern Nigeria4.

4 Details of the sampling procedure can be found on pages 20-22 of Ataguba et al., (2008)

which is available online at www.pep-net.org/programs/pmma/working-papers.

AFRICAN REVIEW OF MONEY FINANCE AND BANKING - 2010

Nsukka LGA is located in the northern part of Enugu State, Southeastern

Nigeria. It is made up of 15 communities with a population estimate ofabout 309,633 inhabitants. Malaria, TB, diarrhoea, and respiratory infectionsrank as the top public health concerns in Nsukka (Ichoku et al., 2010). The in-creasingly low level of care by the rural population has adverse effects onthe health and economic productivity of the people. The increasingly lowlevel of care is largely driven by their low purchasing power, hence their po-tential inability to finance health care needs when household members fallill. It is recorded that only about 59% of pregnant women in Nsukka LGAseek antenatal care. Furthermore, it is estimated that the average monthlycost of treatment for common diseases ranges from $4.4 to $15 per capita forthose who are ill (Onwujekwe and Uzochukwu, 2005). Malaria treatmentalone would cost households about $14 per capita, TB about $7.7 per capitaand the poor spend relatively large amounts as a proportion of their incomeI on treatment (Onwujekwe and Uzochukwu, 2005). These differences inhealth and health care payments in the area points to the necessity for pre-payment schemes to cater for the poor.

The questionnaire was administered by trained enumerators to house-

hold heads in the local language (Igbo) of the community. It was divided in-to two broad categories. The first category elicited information on house-holds’ socio-economic and demographic characteristics, health status, assetsholding, housing and wealth information, community variables as well as,community willingness to participation in financing the scheme.

The second mainly focused on the contingent valuation scenario under

which the evaluation of the proposed CHI scheme took place. This scenariodetailed the nature of the new CHI initiative being proposed in Nsukka, thecurrent health service delivery situation in Nsukka, the institutional settingin which the proposed scheme will be provided, and how each householdwill have to pay to finance the scheme (i.e., in-kind quarterly contributions). In the WTP question, respondents were asked if the only available option topay for the scheme was through in-kind contribution: would he/she be will-ing to contribute? For those who said no, they were asked to give reasons fornot wanting to pay to help finance the scheme. However, for those who ac-cepted, they were asked to list the maximum quantities of agricultural com-modities they were willing to contribute quarterly to finance the scheme.5

5 The scale of measurement was a local market basket called ‘the mudu’. Most households

stated their contributions in terms of rice, beans, cassava, maize, yams, pears, etc. The listedcommodities were then converted into actual cash using their current market values to arrive attheir monetary equivalence or WTP values for the sampled households.

W.M. FONTA, H.E. ICHOKU & J.E. ATAGUBA - PAYING FOR CBHIS IN RURAL NIGERIA USING IN-KIND PAYMENTS

Overall, out of a total of 380 households randomly selected for interview, 309were successfully interviewed either during the first visit or during a followup visit while 71 households refused outright to be interviewed. 4. THE ECONOMETRIC MODEL

Our prime interest here is to identify the determinants of households’

WTP for the scheme. However, for this amount to be observed, a householdmust first be willing to participate in financing the scheme. The situationtherefore warrants a joint decision process, first involving whether or not ahousehold decides to participate in financing the scheme (i.e., participationmodel), and secondly; having decided to participate, the actual amounthe/she is willing to pay (i.e., valuation model). If we estimate the determi-nants of WTP for the scheme based only on the sub-sample of those with re-ported WTP values, it could be incorrect if there is bias introduced by self-se-lection of individuals into the participation model (Strazzera et al., 2003). Thus, to check the presence of sample selection bias, we modelled the twochoices simultaneously using Heckman’s 2-step approach.

Formally, let Y1 denotes the WTP amount for the scheme, and Y2 for a bi-

nary variable assuming the value of 1 if a household decides to participate inthe scheme and 0 otherwise (i.e., no WTP amount). Let x and w also repre-sent vectors of explanatory variables for the valuation and participationmodels such as respondent age, education level of household head, house-hold income, household size, household poverty status, gender of the re-spondent, household composition, the health status of the respondent, previ-ous participation in a social health insurance initiative, cost of treatment,means of treatment, distance and quality of available health care facilities6. Then we can write:

for the (log) WTP equation, where σ is a scale factor, Y1i is observed only

6 These hypothesized variables are based on findings from social health insurance schemes.

These include studies by Asenso-Okyere et al., (1997); Dong et al., (2003a & 2003b, 2004a & 2004b& 2005); Binam et al., (2004); Jiang et al., (2004); Asfaw and Braun, (2004); Fonta and Ichoku(2005); Basaza et al., (2008); Ataguba et al., (2008) & Onwujekwe et al., (2010, 2011) etc.

AFRICAN REVIEW OF MONEY FINANCE AND BANKING - 2010

for the participation equation. The joint distribution of (εi,μi) is assumed to

be bivariate normal with zero means, variances equal to 1 and correlation ρ. When ρ = 0 the two decisions are independent and the parameters of the twoequations can be estimated separately (Strazzera et al., 2003). The Heckmanprocedure is carried out in two stages. First, note that the conditional expect-ed value of (Y1i) is:

1i Y2i = 1] = x’i + ρσλ(w’i )

i ) = φ (w’i )|Φ (w’i ) is the inverse of the Mills ratio and φ and Φ are

the standard normal density and standard normal functions, respectively. Thefirst step of the Heckman procedure entails the estimation of the participationequation by Probit, which gives us an estimate of λ. The second step consistsof a least squares regression of Y1i on x and λˆ (i.e., valuation equation). 5. EMPIRICAL RESULTS 5.1 Sample Statistics

Table presents the description and summary statistics of the sampled

population. On average there are 6 members in a household. Most of thehousehold heads interviewed (99%) were employed by the Local Govern-ment Authority (mainly as menial labourers and clerks) or in the informalsector as craftsmen, petty-traders and farmers. Note that because of the pres-ence of informal sector workers we rather used wealth index as a proxiedvariable for income as discussed in Fonta (2006). Hence, the average incomefor the sample was calculated at NGN121,714.20 or about US$936.267 per an-num or NGN10,142.85 (US$ 78) per month. In terms of gender distribution,more than 63% of the sampled household heads were male. Further still, theaverage age of the household head in the survey was about 52 years withover 77% having more than 7 years of formal education. Conversely, about78% of respondents expressed confidence in the proposed scheme while theaverage cost of treatment for common diseases was about NGN763 orUS$5.87 across the whole sample. Likewise, the average amount borrowedfor treatment, including money obtained from the sale of valuable assets and

7 As at the time of survey, the exchange rate stood at US$1 NGN130.

W.M. FONTA, H.E. ICHOKU & J.E. ATAGUBA - PAYING FOR CBHIS IN RURAL NIGERIA USING IN-KIND PAYMENTS

property across all respondents was estimated to be about NGN666 orUS$5.12. This is equivalent to over 87% of the amount spent on treatmentacross all respondents. Furthermore, more than half (60.2%) of the sampledhousehold heads reported their health status as being better than ‘Good’ atthe time of interview. Equally, about (55%) of the sample reported seekinghealth care services from orthodox8 health care providers while about 45%reported patronizing patent medicine dealers. Finally, in terms of havingknowledge about health insurance or any other form of insurance, the sam-ple response rate was quite low. Only about 11% reported having health in-surance knowledge or knowledge about any form of health insurance. Table 1: Description of the variables used in analysis Variable Definition and Measurement Proportion*

The Age of the respondent at the last birthday (in years)

Gender of household head 1 = male and 0, otherwise

Education attainment of household head = 1 >

Knowledgeable about health insurance or any form

of insurance 1 = knowledgeable and 0, otherwise

Nature of floor material 1 = cement/tiles/concrete

Ownership of toilet facility 1 = own and 0, otherwise

Ownership of bathroom 1 = own and 0, otherwise

The total number of rooms in the occupied building

excluding the living/dining room, kitchen,toilets and bathrooms

Proxy measure for income level of households.

This includes considering durable assets, household

building materials, ownership of livestock, economictrees, etc. which are further converted into theircurrent market value using current market prices. The market prices used were obtained as the amountit will cost the household to sell the items.

8 Orthodox providers are categorized as clinics, maternity centres, dispensary, and hospi-

tals. The unorthodox providers are categorized as patent medicine stores, traditional healersand herbalists, etc.

AFRICAN REVIEW OF MONEY FINANCE AND BANKING - 2010

Total number of household members living together

usually as a nuclear family unit (Household size)

Indicating whether or not any household member

fell ill in the past two weeks prior to interview and1 = sick and 0, otherwise

Dichotomous variable indicating whether or not

the individual accepts to contribute1 = accept and 0, otherwise

Whether the respondent is employed or not both

in the formal and informal sector 1 = employedand 0, otherwise

Indicating whether or not the respondent or any

household member had previously participated in anyhealth insurance initiative or are currently enrolledin one. 1 = participated/participating and 0, otherwise

The general state of health of the respondent at the

time of interview 1 = Poor; 2 = Fair; 3 = Good;

The general and often ‘usual’ means of seeking

treatment when any member of the householdfalls ill 1 = orthodox and 0, otherwise

The general rating of the quality of the health centres

nearest to the respondent 1 = Poor; 2 = Fair; 3 = Good;

Nature of dwelling defined by the building and

construction materials used 1 = cement/concreteand 0, otherwise

Indicating the level of confidence in any community

trust fund or where funds are pooled together and

managed by the community 1 = Highly distrust;

2 = Distrust; 3 = Trust; 4 = Highly trust

Amount spent on treatment of any household member

during the past four weeks. This includes thequantifiable indirect and direct costs measured in Naira.

W.M. FONTA, H.E. ICHOKU & J.E. ATAGUBA - PAYING FOR CBHIS IN RURAL NIGERIA USING IN-KIND PAYMENTS

Amount borrowed for the treatment of any household

member during the past four weeks where any

household member has fallen sick. This also includesthe monetary worth (measured in Naira) of sold items.

The distance from the household to the nearest health

centre measured to the nearest Kilometres. 5.2 Empirical Results

Out of a total of 380 households randomly selected for interview, 309

were successfully interviewed either during the first visit or during a followup visit. The remaining 71 households (18.7%) were mainly those which re-fused outright to be interviewed. The reasons behind survey refusals in gen-eral have been extensively discussed in the sample survey literature (see, fore.g., Cochran, 1977; Mitchell and Carson, 1989; Deaton, 1997; Amahia, 2010 &Okafor, 2010). However, besides the refusals, there are also householdswhich agreed to participate in the survey but however, reported a zero valuefor the scheme (i.e., ‘protest’ zeros or bidders). This behaviour may be as-cribed to a variety of reasons such as free riding (loading), adverse reactionto the interview in general or in particular to the mode of payment adoptedin the study (Strazzera et al., 2003 & Fonta et al., 2010). Of a total of 309 re-spondents which actually participated in the survey, 264 respondents(79.7%) provided positive responses to the valuation question while about 63respondents (20.3%) protested against the proposed community trust fundwhere contributions were to be pooled to finance the scheme.

It was therefore necessary to determine whether excluding protest bid-

ders from the econometric analysis would lead to a sample selection biasproblem. As noted in Mekonnen (2000); Strazzera et al., (2003); Fonta andOmoke (2008) & Fonta et al., (2010), a preliminary test for sample selectionbias is to compare the means of household covariates between the twogroups (i.e., positive versus protest bidders) using t-statistics. Any significantdifference between both groups of respondents is an early warning indicatorof the presence of sample selection bias. For most of the considered variablesin the study (Table 1), we found no significant differences between positiveand protest bidders at both 1% and 5% levels of confidence. However, to becompletely certain that the results were theoretically plausible and statisti-cally satisfactory in terms of sample selection bias, Heckman’s 2-step estima-tor was used for further diagnostic. The results are reported in Table 2.

AFRICAN REVIEW OF MONEY FINANCE AND BANKING - 2010

Table 2: Heckman’s 2-step Estimates Part. Model (2) Val. Model (3) Variable Std. Err. Std. Err.

LR chi 2 (3) = 19.03; Prob > chi 2 = 0.0009

Significance of parameters * < 0.10, ** < 0.05, *** < 001. Table 3: Summary of estimated mean quarterly WTP amount (in Naira) CI-Median

W.M. FONTA, H.E. ICHOKU & J.E. ATAGUBA - PAYING FOR CBHIS IN RURAL NIGERIA USING IN-KIND PAYMENTS

Starting first with the Probit results to explain included versus excluded

households in the participation model, sickness seems to have an effect onthe probability to participate or not. In particular, being positive, implies thathousehold members that fell sick two weeks prior to the survey had higherparticipation rate. This may perhaps be because implementing the scheme inthe area is expected to improve health care delivery services and hence,household health status. Similarly, distance also had an effect on the decisionto participate or not and being negative, implies that the further away ahousehold is from a health facility the greater the probability to participate. Possibly because the further away a household is from the nearest healthcenter, the higher the cost of transportation and frequency of visits is lower. This may explain why such households are more willing to pay to financethe scheme than those living closer to existing healthcare facilities. Equally,education also had an effect on the participation rate. Higher educationalachievement seems to induce higher participation rate. This may perhaps bebecause people who are more educated are likely to be more knowledgeableabout health insurance and its benefits and are therefore more willing to payfor it. Finally, individuals who perceived the quality of the available healthcenters nearest to them as being fair, good, and very good, had a better dis-position to participate since the proposed scheme is meant to improve, sup-ply and utilize existing health care facilities.

In the valuation equation where ln(WTP) is the dependent variable, rich-

er households are willing to pay higher amounts than poorer householdheads as also reported by Dong et al., (2003a), Binam et al., (2004) and Asgaryet al., (2004) although Asenso-Okyere et al. (1997) reported a negative rela-tionship. In the study reported here, the amount households are willing topay is an increasing function of their ability to pay. Ceteris paribus, maleheaded households are willing to pay higher amounts than female headedhouseholds, a finding also reported by Dong et al., (2003b). This could belinked to the roles of men in the community who have traditionally beencharged with the responsibility of catering for the family financially. Similar-ly, larger households are also willing to pay higher amounts than smallerhouseholds. This is likely to be as a result of the potentially greater financialburden faced by larger households when they seek health care. Further,households that perceived the quality of the healthcare centres nearest tothem as being ‘poor’ are willing to pay more than households that perceivethe quality to be good. This is probably due to the deprivation suffered in ac-cessing health care. Furthermore, household heads that have greater trustand confidence in the proposed scheme are willing to pay higher amountsthan those who have low confidence in the scheme. This has also been ob-

AFRICAN REVIEW OF MONEY FINANCE AND BANKING - 2010

served by Basaza et al., (2008) and judged by them to be an important consid-eration for the success of community health financing schemes. Finally, sincethe coefficient on is not significantly different from zero, there is no indica-tion of a sample selection bias. 5.3 WTP Predictions

On the basis of the fact that there is no significant evidence of sample selec-

tion bias, we used the modelling results for the sub-sample of positive respon-dents to predict the mean WTP estimate for the scheme. The predicted esti-mates are reported in Table 3. The mean and median quarterly WTP amountsfor the scheme were computed as N1010 (US$7.77) and N852 (US$6.55) respec-tively. These estimates seem intuitively reasonable, although they are smallcompared with N763 (US$5.87) per month spent on treatment per householdas observed by Asfaw and Braun (2004). However, this is not a major problemwhen using the CVM device to inform the design of CHI schemes. As earlierindicated, one major advantage of using the method is that the mean or medi-an WTP estimates obtained can be used as a basis for computing the aggregateWTP of the financing community. The aggregated amount can therefore becompared with the actual cost of financing the scheme. If, however, there isneed for additional funding as in the case with the current application, thenthe local authorities can solicit for support from counterpart funding, grants,or subvention from the government or donor agencies. 6. CONCLUSION

The proposed policy of the Government of Nigeria to bring health care

closer to the people through the new National Health Insurance Scheme(NHIS) is potentially very important. However, a major concern by many isthat the new NHIS seems to focus more on the formal sector than the informalsector. While conventional wisdom suggests that it is certainly easier to reachpeople in formal employment than those in the informal sector, the fact stillremains that many Nigerians work in the informal sector and are therefore indire need of urgent social healthcare protection. The seeming lack of commit-ment by central government to provide social healthcare protection for thepoor has led to calls for ways to protect the poor from the high cost of medicalpayments especially the increasing level of out of pocket payments (OOPs) bydifferent levels of sub-national governments in Nigeria using CBHIS.

However, the design and implementation of successful CBHIS in many

communities of Nigeria, has proven to be a very difficult task for many

W.M. FONTA, H.E. ICHOKU & J.E. ATAGUBA - PAYING FOR CBHIS IN RURAL NIGERIA USING IN-KIND PAYMENTS

healthcare policy planners in the country. This may be partly as a result ofthe lack of knowledge of existing participatory methodology that can helpelicit important project information from host communities. The main pur-pose of this study was therefore, to design an improved planning methodol-ogy that could elicit household WTP for an intended CBHIS in the NsukkaLocal Government Area of Enugu state, Nigeria, and to inform the local au-thorities in setting appropriate household insurance premiums or levies. Inthe application context, we find that CVM can be successfully used to sup-port the design and implementation of CBHIS and that analysis of the valua-tion function can provide qualitative information that is difficult to identifyusing alternative health evaluation techniques. For instance, the empiricalfindings produced a mean quarterly WTP amounts for the scheme of aboutN1,010 ($7.77). This amount could be used by the local authority to designthe appropriate household insurance premium or levy for the scheme. Alter-natively, it could be used as the basis for calculating the community’s aggre-gate WTP for the scheme. The aggregated amount can therefore be com-pared with the actual cost of financing the scheme in the area.

We conclude that if health care financing is to meet the objectives of equity

in financing and access to health care services and also to guarantee access tothe delivery of quality care, such a financing mechanism must have an insur-ance function built into it and a higher degree of risk pooling. In the case con-sidered in this paper, this scheme is best seen as an interim step for the poorwhile the National Health Insurance Scheme (NHIS) is developed more fully. Acknowledgements

This paper was prepared while the first author was a visiting scholar at UNU-INRA,under the Centre for Environmental Economics and Policy in Africa (CEEPA), visit-ing fellowship for Africans working in the area of Environmental Economics. Thework was carried out with financial and scientific support from the Poverty and Eco-nomic Policy (PEP) Research Network, which is financed by the Australian Agencyfor International Development (AusAID) and the Government of Canada through theInternational Development Research Centre (IDRC) and the Canadian InternationalDevelopment Agency (CIDA). The field work exercise was funded by the SwedishInternational Cooperation and Development Agency (SIDA). The author also ac-knowledges the useful comments by Profs. Gavin Mooney, Jean-Yves Duclos, SteveYounger, Habiba Djebbari, Edina Sinanovic, Araar Abdelkrim and other discussantsand members of the PEP network that helped to shape the work. We also acknowl-edge helpful comments from an anonymous reviewer. The initial version was accept-ed for presentation at the University of Oxford Centre for Study of AfricanEconomies (CSAE), March 16-18, 2008. The usual disclaimer applies.

AFRICAN REVIEW OF MONEY FINANCE AND BANKING - 2010

References

Akin S., N. Birdsall, and M.D. De Ferranti, 1987, Financing Health Services in Develop-ing Countries: An Agenda for Reform, A World Bank Policy Study, Washington: TheWorld Bank.

Amahia G.N., 2010, “Factors, Preventions and Correction Methods for Non-Response

in Sample Survey”, CBN Journal of Applied Statistics, Vol. 1, No. 1, pp. 79-89.

Arhin-Tenkorang D., 2001, “Health Insurance for the Informal Sector in Africa: De-

sign Features, Risk Protection and Resource Mobilisation”, CMH Working PaperSeries.

Asenso-OkyereW.K., I. Osei-Akoto, A. Anum and E.N. Appiah, 1997, “Willingness to

Pay for Health Insurance in a Developing Economy: A Pilot Study of the InformalSector of Ghana Using Contingent Valuation”, Health policy, Vol. 42, pp. 223-237.

Asfaw A. and J. Braun, 2004, “Can Community Health Insurance Schemes Shield the

Poor Against the Downside Health Effects of Economic Reforms? The Case of Ru-ral Ethiopia”, Health policy, Vol. 70, pp. 97-108.

Asgary A., K. Willis, A.A. Taghvaeli and M. Rafeian, 2004, “Estimating Rural House-

holds’ Willingness to Pay for Health Insurance”, The European Journal of HealthEconomics, Vol. 5, pp. 209-215.

Ataguba J.E., 2006, “An Estimation of The Willingness to Pay for Community Health-

care Risk-Sharing Prepayment Schemes: Evidence from Rural Nigeria”, An Un-published dissertation Submitted to the University of Cape Town.

Atagbuba J.E, H.E. Ichoku and W.M. Fonta, 2008, “Estimating the Willingness to Pay

for Community Healthcare Insurance in Rural Nigeria”, Poverty and Economic Pol-icy Research Network PMMA Working paper, No. 2008-10.

Basaza R., B. Criel and P. Vander Stuyft, 2008, “Community Health Insurance in

Uganda: Why Does Enrolment Remain Low?: A View from Beneath”, Health Poli-cy, Vol. 87, pp. 172-184.

Bennett S., A. Creese and R. Monasch, 1998, “Health Insurance Schemes for People

Outside Formal Sector Employment”, World Health Organization (WHO), Divisionof Analysis, Research and Assessment (ARA).

Binam J., A. Nkama and R. Nkenda, 2004, “Estimating the Willingness to Pay for

Community Health Prepayment Schemes in Rural Area: A Case Study of the Useof Contingent Valuation Surveys in Centre Cameroon. Retrieved”, August 12,2005, from: http:// www.csae.ox.ac.uk/conferences/2004-GPRaHDiA /papers/4h-Binam-CSAE2004.pdf.

Bitran R.A. and U. Giedon, 2003, “Waivers and Exemptions for Health Services in De-

veloping Countries”, Social Protection Discussion Paper Series, No. 0308, Social Pro-tection Unit, Humand Development Network, Washington: The World Bank.

Brieger W.R. and O. Alubo, 2002, ‘‘Clarifying the Case on the Role and Limitations of

Private Health Care in Nigeria”, Health Policy and Planning, Vol. 17, pp. 218-220.

W.M. FONTA, H.E. ICHOKU & J.E. ATAGUBA - PAYING FOR CBHIS IN RURAL NIGERIA USING IN-KIND PAYMENTS

Carrin G., 1987, “Community Financing of Drugs in Sub-Saharan Africa”, The Inter-national Journal Health Plan Management, Vol. 2, No. 2, pp. 125-145.

Cochran G.W., 1977, Sampling Techniques, New York: John Wiley & Sons.

Criel B. and M.P. Waelkens, 2003, “Declining Subscriptions to the Maliando Mutual

Health Organisation in Guinea-Conakry (West Africa): What is Going Wrong?”,Social Science and Medicine, Vol. 57, pp. 1205-1219.

Cripps G., J. Edmond, R. Killian, S. Musau, P. Satow and M. Sock, 2000, “Guide to

Designing and Managing Community-Based Health Financing Schemes in Eastand Southern Africa: Including Toolkit”, Version 1, Partnerships for Health Reform,Abt Associates Inc., Bethesda, MD.

Davies P. and G. Carrin, 2001, “Risk-Pooling: Necessary But not Sufficient?”, Bulletinof the World Health Organization, Vol. 79, No. 7, p. 587.

De Allegri M., M. Sanon, J. Bridges and R. Sauerborn, 2006, “Understanding Con-

sumers’ Preferences and Decision to Enrol in Community-Based Health Insurancein Rural West Africa”, Health policy, Vol. 76, pp. 58-71.

Deaton A., 1997, The Analysis of Household Surveys, The Johns Hopkins Univ. Pr Balti-

Dong H., B. Kouyate, J. Cairns, F. Mugisha and R. Sauerborn, 2003a, “Willingness-To-

Pay for Community-Based Insurance in Burkina Faso”, Health Economics, Vol. 12,pp. 849-862.

Dong H., B. Kouyate, J. Cairns, F. Mugisha and R. Sauerborn, 2004a, “Differential

Willingness of Household Heads to Pay Community-Based Health Insurance Pre-mia for Themselves and Other Household Members”, Health Policy and Planning,Vol. 19, pp. 120-126.

Dong H., B. Kouyate, J. Cairns, F. Mugisha and R. Sauerborn, 2005, “Inequality in

Willingness-To-Pay for Community-Based Health Insurance”, Health Policy, Vol. 72, pp. 149-156.

Dong H., B. Kouyate, R. Snow, F. Mugisha and R. Sauerborn, 2003b, “Gender’s Effect

on Willingness-To-Pay for Community-Based Insurance in Burkina Faso”, HealthPolicy, Vol. 64, pp. 153-162.

Dong H., F. Mugisha, A. Gbangou, B. Kouyate and R. Sauerborn, 2004b, “The Feasi-

bility of Community-Based Health Insurance in Burkina Faso”, Health Policy, Vol. 69, pp. 45-53.

Dror D.M. and A.S. Preker, 2002, Social Reinsurance: A New Approach to SustainableCommunity Health Financing, Washington, DC: The World Bank.

Ekman B., 2004, “Community-Based Health Insurance in Low-Income Countries: A

Systematic Review of the Evidence”, Health Policy and Planning, Vol. 19, pp. 249-270.

Fafchamps M., 2003, Rural Poverty, Risk and Development, Edward Elgar Publishing.

Heinzen R.R. and J.F.P. Bridges, 2008, “Comparison of Four Contingent Valuation

AFRICAN REVIEW OF MONEY FINANCE AND BANKING - 2010

Methods to Estimate the Economic Value of a Pneumococcal Vaccine inBangladesh”, International Journal of Technology Assessment in Health Care, Vol. 24,No. 4, pp. 481-487.

Fonta M.W. and E.H. Ichoku, 2005, “The Application of the Contingent Valuation

Method to Community-Led Financing Schemes: Evidence from Rural Cameroon”,Journal of Developing Areas, Vol. 39, No. 1, pp. 106-126.

Fonta W.M., 2006, “Valuation of Community-Based Financing of Environmental Proj-

ects: A Case Study of Malaria Control in Bambalang, Cameroon”, PhD Thesis, En-vironmental Economic Unit, Department of Economics, University of Nigeria,Nsukka.

Fonta M.W. and P. Omoke, 2008, “Testing and Correcting for Sample Selection Bias in

Social Science Research: Application to Contingent Valuation Method (CVM) Sur-vey Data”, European Journal of Social Sciences, Vol. 6, No. 2, pp. 232-43

Fonta M.W., E.H. Ichoku, K.K. Ogujiuba and J.O. Chukwu, 2008, “Using a Contingent

Valuation Approach for Improved Solid Waste Management Facility: Evidencefrom Enugu State, Nigeria”, Journal of African Economies, Vol. 17, No. 2, pp. 277-304.

Fonta M.W. and H.E. Ichoku, 2009, “La Valeur De La Gestion Des Déchets Urbains:

Constatations Tirées De l’État d’Enugu au Nigéria”, Canadian Journal of Develop-ment Studies, Vol. 28, No. 3-4, pp. 383-396.

Fonta M.W., H.E. Ichoku and J. K-Mariara, 2010, “The Effect of Protest Zeros on Esti-

mates of Willingness to Pay in Healthcare Contingent Valuation Analysis”, Ap-plied Health Economics and Health Policy, 8(4):225-237.

Fonta M.W., E.H. Ichoku and E.O. Nwosu, 2011, “Contingent Valuation in Communi-

ty-Based Project Planning: The Case of Lake Bamendjim Fishery Re-Stocking inCameroon”, AERC Research Paper, No. 210, African Economic Research Consor-tium, Nairobi, Kenya.

FOS 2004, National Living Standard Survey (NLSS) 2003/2004, Abuja, Nigeria, Federal

Jlang Y., A. Asfaw and J. Von Braun, 2004, “Performance of Existing Rural Coopera-

tive Medical Scheme and Willingness to Pay for the Improved Scheme”, Availablefrom: http://www.tropentag.de/2003/abstracts/full/104.pdf.

Johnnesson M., 1996, “A Note on the Relationship Between Ex Ante and Expected

Willingness to Pay for Health Care”, Social Science and Medicine, Vol. 42, pp. 305-311.

Mathiyazhagan K., 1998, “Willingness to Pay for Rural Health Insurance Through

Community Participation in India”, International Journal of Health Planning andManagement, Vol. 13, pp. 47-67.

Mekonnen A., 2000, “Valuation of Community Forestry in Ethiopia: A Contingent

Valuation Study of Rural Households”, Environment and Development Economics,Vol. 5, pp. 289-308.

W.M. FONTA, H.E. ICHOKU & J.E. ATAGUBA - PAYING FOR CBHIS IN RURAL NIGERIA USING IN-KIND PAYMENTS

Mitchell R.C. and R. Carson, 1989, “Using Surveys to Value Public Goods: The Con-

tingent Valuation Method”, Washington, D.C.: Resources for the Future.

Miladovsky P. and E. Mossialos, 2008, “A Conceptual Framework for Community-

Based Health Insurance in Low-Income Countries: Social Capital and EconomicDevelopment”, World Development, Vol. 36, pp. 590-607.

Musau S.N., 1999, “Community-Based Health Insurance: Experiences and Lessons

Learned from East and Southern Africa”, Report No. 34, Bethesda (MD), Partner-ships for Health Reform Project, Abt Associates Inc.

NBS, 2007, Federal Republic of Nigeria: 2006 Population Census, National Bureau of Sta-

Okafor F.C., 2010, “Addressing the Problem of Non-Response and Response Bias”,

CBN Journal of Applied Statistics, Vol. 1, No. 1, pp. 91-97.

Onwujekwe O.E., E.N. Shu and P. Okonkwo, 1998, “Willingness to Pay for Communi-

ty-Based Ivermectin Distribution: A Study of three Onchocerciasis-Endemic Com-munities in Nigeria”, Tropical Medicine and International Health, Vol. 3, No. 10, pp. 802-808.

Onwujekwe O.E. and B.C. Uzochukwu, 2005, “Socio-Economic and Geographic Dif-

ferentials in Costs and Payment Strategies for Primary Health Care Services inSoutheast Nigeria”, Health Policy, Vol. 71, No. 3, pp. 383-397.

Onwujekwe O.E., E.N. Shu and P. Okonkwo, 2000, “Community Financing of Local

Ivermectin Distribution in Nigeria: Potential Payments and Cost-Recovery Out-look”, Tropical Doctors, Vol. 30, pp. 91-94.

Onwujekwe O., C. Onoka, B. Uzochukwu, C. Okoli, E. Obikeze and S. Eze, 2009, “Is

Community-Based Health Insurance an Equitable Strategy for Paying for Health-care? Experiences from Southeast Nigeria”, Health Policy, Vol. 92, pp. 96-102.

Onwujekwe O., B. Uzochukwu and J. Kirigia, 2011, “Basis for Effective Community-

Based Health Insurance Schemes: Investigating Inequities in Catastrophic Out-of-Pocket Health Expenditures, Affordability and Altruism”, African Journal of HealthEconomics, Vol. 0001, pp. 1-11.

Preker A.S., G. Carrin, D. Dror, M. Jakab, W. Hsiao and D. Arhin- Tenkorang, 2002,

“Effectiveness of Community Health Financing in Meeting the Cost of Illness”,Bulletin of the World Health Organization, Vol. 80, pp. 143-150.

Strazzera E., M. Genius, R. Scarpa and G. Hutchinson, 2003, “The Effect of Protest

Votes on the Estimates of WTP for Use Values of Recreational Sites”, Environmen-tal and Resource Economics, Vol. 25, pp. 461-476.

Udry C., 1994, “ Risk and Insurance in a Rural Credit Market: An Empirical Investi-

gation in Northern Nigeria”, Review of Economic Studies, Vol. 61, pp. 495-526.

WHO, 2000, The World Health Report 2000 - Health Systems: Improving Performance,

AFRICAN REVIEW OF MONEY FINANCE AND BANKING - 2010

Résumé:

Soins de santé de financement pour les pauvres est un défi majeur auquel sontconfrontées populations les plus pauvres de la planète dans les pays en développe-ment. Alors que plus de 90% de la charge mondiale de morbidité est supportée parplus de 80%, seulement environ 11% des dépenses de santé mondiale est sur les pau-vres. Communauté des régimes d’assurance santé (CBHIS) ont émergé en Afriquepour mobiliser les ressources communautaires. Ils peuvent aussi être un tremplin versune couverture plus formelle et potentiellement universelle. Dans certaines régionsd’Afrique où de tels régimes existent, ils n’ont pas effectivement couvert la popula-tion cible. Le Nigeria a quelques programmes tels. Ce document utilise l’évaluationcontingente d’examiner la possibilité d’adopter CBHIS utilisant des paiements en na-ture dans les régions rurales du Nigeria. L’étude constate que le sexe, la taille du mé-nage, l’état de santé, la qualité des centres de soins de santé, la confiance dans le sys-tème proposé, la distance du centre de soins de santé le plus proche et le revenu sontdes déterminants majeurs de la volonté des ménages à payer (CAP) pour le régime. Mots-clés: Financement des soins de santé, pauvres en milieu rural; CBHIS; CAP, des paiements en nature, le Nigeria.

The Effects of the Chiropractic Adjustment. Recently there has been a growing attack on chiropractic and children launched by foes of our profession and some misguided practitioners. The reason and rational as to why children can benefit from chiropractic care is simple: Life is a process. Health is a process. Disease is a process. Healing is a process and Wellness is a process that encompasses

10 kinds of homemade tea practices and effectiveness ginseng: sex more peaceful, not warm but not dry, either qi, but also fluid, suitable for rousing,enhance physical fitness and anti- disease capabilities. White ginseng (sugar ginseng): more choice of body short, inferior quality of ginseng, blanched inboiling water cook for a while, soaked in syrup, then dried. White ginseng (ginseng sug

AFRICAN REVIEW OF MONEY FINANCE AND BANKING - 2010

al., (1997); Asfaw and Braun (2004); Dong et al., (2004b); Binam et al., (2004);Fonta 2006; Basaza et al., (2008); Ataguba et al., (2008) & Onwujekwe et al.,(2010 & 2011), to inform the design and initiation of CHI schemes in Ghana,Ethiopia, Burkina Faso, Cameroon, Uganda and Nigeria respectively. How-ever, as earlier indicated, most of these studies with the exception of Asfawand Braun (2004), failed to explore the importance of using in-kind contribu-tions as a viable community financing option.

AFRICAN REVIEW OF MONEY FINANCE AND BANKING - 2010

al., (1997); Asfaw and Braun (2004); Dong et al., (2004b); Binam et al., (2004);Fonta 2006; Basaza et al., (2008); Ataguba et al., (2008) & Onwujekwe et al.,(2010 & 2011), to inform the design and initiation of CHI schemes in Ghana,Ethiopia, Burkina Faso, Cameroon, Uganda and Nigeria respectively. How-ever, as earlier indicated, most of these studies with the exception of Asfawand Braun (2004), failed to explore the importance of using in-kind contribu-tions as a viable community financing option.