He encontrado que alguna farmacia puede tener existencias limitadas de ciertos medicamentos, mientras que otras pueden tener casi cualquier formato que se le ocurra y el habitual de dosis habitualidad apareció. En resumen, siempre se contiene el almacén de corroborar. Al mismo tiempo que el producto que más que gustaba ha resultado no estaba disponible en stock otro distinto por las Buenas costumbres también debe buscarse jefe no asн parezca. Por eso es importante disponer de un Plan B para actuar cuandod ello no ocurra.

Ventaja de tomar un genérico en lugar de Asix

Un genérico es más barato que el nombre de marca

Uno de los mayores incentivos para someterse al Dónde comprar Lasix genérico en lugar de pagar la marca es que usted puede obtener un ahorrando importantes Lasix genérico. Por lo tanto, un Lasix genérico es en general mucho más barato que el homólogo de marca, así que una denominación genérica se hace posible para las personas que usan este medicamento con frecuencia. Un ejemplo: La compra de lurosemida en lugar de Lasix es una considerable ahorro para el presupuesto mensual de medicamentos.

Ma32

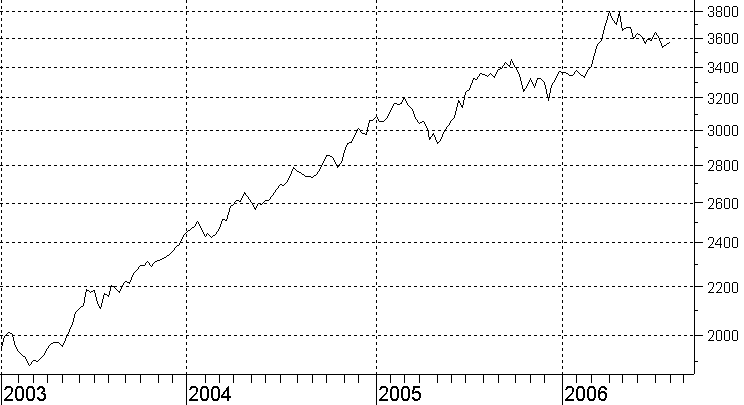

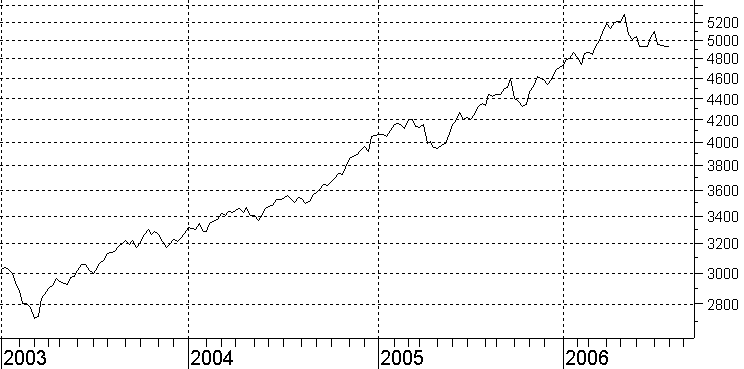

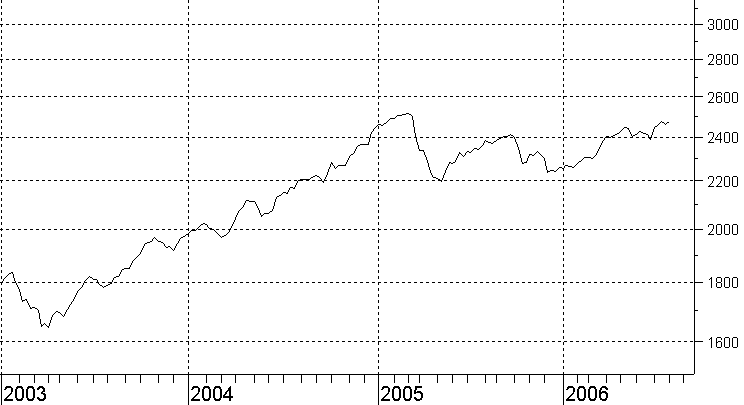

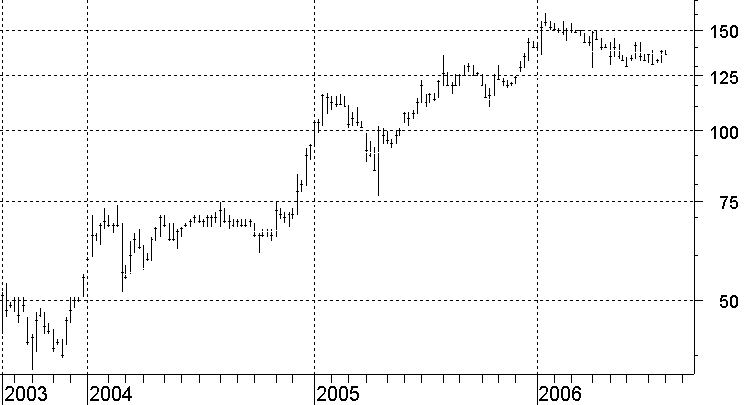

Twenty Five Years of Independent Information and Unbiased Advice on the Australian and NZ StockmarketsMarketAnalysis

Circadian Technologies realises significant gain . 5

Cellnet Group's financial position improves,

Summary and Recommended Investment Strategy. Our Forecasts for the Australian and New Zealand stockmarkets are just Neutral to slightly Bullish, but many sharesoffer good value and there are signs that smaller company shares are starting to recover. Remain fully invested.

Over the medium to long term smaller company shares

Stockmarket Forecasts

tend to outperform large company shares. There are

several possible explanations for this: Large companies

60% (Neutral) 55% (Neutral)

tend to be mature businesses, so smaller companies have

65% (Bullish) 62% (Bullish)

greater long term growth potential. Or perhaps thereason is simply that large companies are widely followedand therefore fairly valued, while smaller companyshares are often neglected and tend to be under-valued. If you pay less to buy a share (i.e. when it is under-valued) then your long term returns will be higher.

Smaller company shares, however, do not outperform

larger company shares every year. In fact, NZ smaller

company shares have just gone through a four yearperiod when they have under-performed NZ largercompany shares. The reason for this shorter termvariance in performance is fairly apparent. The fortunesof smaller companies tend to be more closely tied to thedomestic economy, while larger companies tend to haveexport markets and/or greater pricing power (e.g. Auckland Airport, Telecom, the power companies) sosuffer less as the domestic economy slows.

Despite the poor performance of smaller company

shares - a sector in which this newsletter often investsheavily - our Recommended Portfolio has far

outperformed even the larger company indices over the

So smaller companies have under-performed over

the last four years anticipating the current economicslowdown. As we have written over recent months,these shares now offer good value, should experiencestronger profit growth when the economy eventuallyrecovers and will probably outperform larger companyshares over the next couple of years as the marketanticipates the next economic upturn.

There are clear signs that this recovery by smaller

company shares has already started, with this sector

strongly outperforming larger company shares over thelast four months. "Performance Forecasts" are computer generated predictions of the relative future price performance of a company's shares over the next three to six months. Performance Forecasts are calculated for every listed NZ share (except Investment Trusts) on a rating scale using the letters "A" (Highest potential for capital appreciation over the next 3-6 months ), "B" (Above Average), "C" (Average), "D" (Below Average) and "E" (Lowest). These predictions are NOT buy or sell recommendations, but can be useful to help time planned purchases or sales, or to identify shares worthy of further study and analysis.

Copyright Securities Research Company Ltd

CDL Investments lifted revenues 27.0% to $11.7 million

two adjoining sites in Christchurch with a total area of

for the six months to 30 June. Profits were 22.1% higher

at $3,797,000 (1.8 cents per share) and there was a cash

Historically CDL Investments has focused on the

residential market but to “further maximise returns on

58 sections were sold in the period, down from 66 in

our land assets” has undertaken a feasibility study on “a

the first half of 2005 and 77 in the first half of 2004. The

number of options” for unspecified “diversification and

company reports “an oversupply of sections in some

areas and market segments”, a “current downward market

Renaissance Corporation reports revenues up

cycle” and difficult trading conditions. Nevertheless,

11.4% to $77.5 million for the six months to 30 June,

CDL Investments has continued to trade profitably

with profits up 18.5% to $2,293,000 (5.9 cents per

despite the decline in the number of sections sold over

share). The interim dividend will be 12.5% higher at 4.5

the last two years. The company remains “confident we

cents per share (plus full imputation tax credits).

can deliver another positive result for 2006”.

The company produced a cash operating deficit of

The company holds conditional contracts to acquire

$4.6 million - mainly owing to (Continued on Page 4)Portfolio of Recommended Investments

The average Total Return (i.e. both Capital Gains/Losses plus Dividends received) of all current investments from initial recommendation is +159.3%. This is equal to an average annual rate of +29.8%, based upon the length of time each position has been held. The average annual rate of gain of ALL recommendations (both the 37 current and 133 closed out) is +32.3%, compared with a market gain of +8.8%(by the SRC Total Return Index). CURRENT ADVICE is either Buy, Hold+, Hold, Hold- or Sell. Hold+ indicates the most attractive shares not rated as Buy. Hold- indicates relativelyless attractive issues. * Initial Recommendation Prices adjusted for Share Splits, Bonus and Cash Issues.

Copyright Securities Research Company Ltd

Recommended Investments (Cont'd from Page 3)

services can vary significantly on a month to month

Renaissance Corporation sees its competitive

Campbell Brothers has increased its holding in CCI

advantage in its “ability to manage brands”,

Holdings from 9.99% to 11.14% through on-market

“warehousing and distribution” and “expertise in

systems, particularly online transactional systems”. It

Campbell Brothers shares have quadrupled in value

has expanded its IT brands to include products from

over the last three years, but market conditions remain

Canon, Tandberg, Foundry and Allot - and it is also

favourable, the Laboratory Services business has a

looking to expand into non-IT durable goods, including

strong competitive advantage and growing economies

of scale as it expands. So we continue to rate the shares

Renaissance Corporation is continuing to forecast an

a strong “Hold+” and are in no hurry to realise profits.

“approximately 20%” increase in profits for the full year

Cellnet Group has briefly reported for the year to 30

June. Revenues rose 7% to $560 million but, as expected,

Australian Shares

profits fell 76% to $1.6 million (about 3 cents per share). (This section is in Australian currency, unless stated.)

Most importantly the restructuring and stock reduction

AJ Lucas Group has acquired McDermott Drilling

has produced a cash operating surplus of $33 million -

Pty, a 35 year old business with “substantial experience

compared with a deficit last year of $18 million which

and expertise in vertical and surface to inseam drilling”

lifted interest bearing debt to dangerously high levels.

for coal mining, coal methane and other industries.

In July Cellnet Group reduced its stock levels by a

Campbell Brothers has acquired Swedish based

further $18 million, with Telecom NZ taking over Analytica AB for $25 million in cash (plus a future

ownership of inventory under the extended distribution

payment of up to $3 million based on performance to

2009). The company has two laboratories in Sweden,

Cellnet Group has yet to publish the full details of

plus customer service centres in Norway and Denmark

this result which will require further analysis to determine

and customers throughout Europe. This acquisition,

the company's improved financial situation. The

plus last year's purchase of Ecochem in the Czech

company, however, states that its balance sheet and

Republic, “provides the depth of management and

working capital situation are “now in excellent shape”

technical staff” to further grow the business in Europe

and it is “well advanced in its review of potential

where it will “now concentrate on organic expansion”,

acquisition targets” which can be funded from “existing

but perhaps with “some small acquisitions”.

Analytica is mainly involved in environmental testing

This result and comments indicate that the company

with “world renowned abilities in analyzing ultra low

has successfully restructured and is now in a position to

trace levels of metals in seawater, waste water, potable

seek growth in the business. The shares appear to be in

water and geological materials”. This technology will

the early stages of a new uptrend, with a Relative

be transferred throughout the group's laboratories “in

Strength rating of +3.3%, ranked 33, so we rate them a

other geographic regions to sell these capabilities to a

“Buy” for both capital appreciation and a high income as

global market”. This is the type of benefit that gives

dividends are likely to be re-instated this year.

Campbell Brothers a major competitive advantage in

The Laboratory Services division now has about

45% of its revenues from assays and chemical analysisand around 50% from environmental services. Thedivision has a 30% global market share in mineralanalysis but only 1% in environmental work - so there isstill excellent potential for expansion!

Campbell Brothers reports that “strong market

conditions have continued into the first quarter” of thecurrent financial year and predict that the half year profitto September 2006 will be 40-50% higher than last year. The company does warn, however, that “demand for our

Copyright Securities Research Company Ltd

Centennial Coal has downgraded its profit forecast

ID projects which should contribute to revenues and

for the year to 30 June 2006 from $20-26 million to

profits in the new financial year (i.e. to June 2007) and

$16-17.5 million, owing to delays at Newstan (which

suffered a pre-tax loss of $48 million for the year) and

In late July the company signed a $14.4 million, six-

localised poor roof conditions at Tahmoor. This level of

year contract to provide managed payment services for

profitability is extremely low, but should improve

the Bank of Queensland. Keycorp will acquire all of

significantly next year so the company plans to maintain

the EFTPOS terminals used by the bank's merchant

customers and progressively replace them with new

Centennial Coal announced a strategic review of its

terminals and software. Keycorp is also seeking to

ownership of the Newstan and several other smaller

finalise a third contract of this type before the end of

mines in February. After receiving indicative bids, the

company has selected a short list of bidders who are

Keycorp has settled a tax dispute relating to a Research

currently conducting due diligence. Final bids are

& Development syndicate established in 1994. Keycorp

expected before the end of September, when a decision

will pay $3,220,000 which is at the lower end of a

regarding this sale - estimated at around $200 million -

potential liability of up to $15 million. Keycorp will

now claim against the parties who provided legal advice

Circadian Technologies owns 22.8% (about 28.5

million shares) of listed Zenyth Therapeutics which is LongReach Group and Allied Technologies have

to be acquired by CSL via a scheme of arrangement.

adjusted the terms of their merger, with the new terms

Under this scheme Zenith Therapeutics' shareholders

being slightly less favourable for the LongReach Group

will receive 86 cents cash per share plus the distribution

investors. Allied Technologies will now issue one share

of listed Avexa shares held by Zenith Therapeutics.

for every 3 LongReach Group shares, instead of for

This will be approximately one Avexa share for every

every 2½ shares. It will also issue one convertible note

for every 3 LongReach Group notes, with the conversion

So Circadian Technologies will receive around $24.5

price increased from 30 cents to 36 cents.

million in cash plus 4.75 million Avexa shares. This

Effectively, LongReach Group is paying 20% more

takeover offers a premium of about 80% over market

to acquire cashed up Allied Technologies, with the

value, boosting Circadian Technologies' net asset value

reverse takeover consolidating every three shares into

by around $12 million or about 30 cents per share.

one new share (and three notes into one new note).

Circadian Technologies' direct holding in Avexa

M.Y.O.B. has acquired New Zealand based Comacc

will rise from 19.4 million shares (13.9% of the company)

for $7 million. Comacc is a supplier of payroll

to around 24.2 million shares (17.3%), while its cash

management solutions for small and medium sized

holding will increase from about $18.5 million to $43

businesses. The company generates annual revenues in

excess of NZ$5 million and earnings (before interest,

We are upgrading Circadian Technologies shares to

depreciation and tax) of around NZ$2 million - making

this a reasonably attractively priced acquisition. Namoi Cotton Co-operative expects the Australian

cotton crop to be around 10% lower this year but to ginaround 795,000 bales (up 2%) and to market about690,000 bales (down 4%). Sonnet Corporation has announced an agreement

with Hewlett-Packard Australia to market to large corporations and Government agencies. Sonnet Corporation will contribute consulting services and Asset Management specialisation, while HP will provide products and services.

Sonnet Corporation's June quarter cashflow statement

shows revenues of $7.1 million and a small operatingcash surplus of $191,000. This is down on the June 2005

International All Sports' cash flow report shows

quarter - which recorded revenues of $13.5 million and

June quarter receipts up 35.0% to $244.7 million

a $3.0 million surplus - but an improvement on the

compared with the same quarter of 2005. Receipts for

previous three quarters which have produced cash

the full year are up 48.3% to $872.2 million. There was

also an annual net cash surplus of $6.3 million, compared

Technology One reports that both the Queensland

with a cash deficit of $1.0 million in 2005. University of Technology and Melbourne's La Trobe

The company also reports “continued increase in

University have each signed multi-million dollar

client receipts and trading turnover” and “trading profits”

contracts to use its Student Management software. These

contributing to its “strong cash reserves” of $29.6 million.

systems will be installed over the next one to two years. Keycorp had downgraded its earnings (before UXC has purchased Infrastructure Construction

interest, depreciation and tax) for the year ended 30 June

Pty, a civil construction business specialising in

2006 from $10-13 million to $9.5 million.

Horizontal Directional Drilling for utilities and

Smartcard sales were weak for the quarter, although

telecommunications companies. The company has a

the company has been working on EMV and government

“strong presence in NSW” (Continued on Page 6)

Copyright Securities Research Company Ltd

Recommended Investments (Cont'd from Page 5)Recommended Portfolio to reflect the 40 cents capital

and will now expand into other states.

repayment. If an investor re-invested that cash on-

UXC has sold Neopurple - a small industrial and

market to buy additional shares then one could have

graphic design studio owned since 1998 but which is

increased shareholdings by around 28%. So we are

assuming that an investor can have 28% more shares for

Vision Systems has changed the conversion terms of

their initial investment in the company. That effectively

its remaining convertible notes to reflect the recent 40

lowers our initial purchase price per share from 68.5

cents capital repayment. Each note will now convert

into 1.2821 ordinary shares. The notes can be converted

Of course, investors over-weighted in Vision Systems

any June or December until December 2008.

shares should probably re-invest in some other portfolio

We have also adjusted our purchase price (and

share, but otherwise it is attractive to acquire further

accumulated dividends) for Vision Systems in our

Computer Selections of NZ Shares based uponour Comprehensive Share Selection Criteria

For an explanation of this table see the Share Selection Methods report sent to all new subscribers or available from our website. These shares are not formal“buy” and “sell” recommendations, but the “Under-Valued”, “Best Performing” and “Income” shares should be considered for purchase, while the “Over-Valued” and “Worst Performing” shares can generally be sold to release money for re-investment in more attractive shares.

Brokers Following NTA Equity ity Ratio Yield Ratio

Brokers Following NTA Equity ity Ratio Yield Ratio

UNDER-VALUED SHARES: Lowest Price/Sales, Yld > 0, Rel Strength > 0

INSIDER BUYING: Most Insider Buying, Relative Strength > 0

OVER-VALUED SHARES: Highest Price/Sales Ratios, Relative Strength < 0

Warehouse Group 470 +11.9 +3.3 12 0-1 6 4.1

BEST PERFORMING SHARES: Strongest Shares, P/E < 20, P/S < 1.0

WORST PERFORMING SHARES: Weakest Shares, P/S Ratio > 0.25, Yield < Twice Average

INCOME SHARES: Highest Yields, Capitalisation > NZ$100 million

0INSIDER SELLING: Most Insider Selling, Relative Strength < 0

Copyright Securities Research Company Ltd

Computer Selections of Australian Shares based uponour Comprehensive Share Selection Criteria

For an explanation of this table see the Share Selection Methods report sent to all new subscribers or available from our website. These shares are not formal“buy” and “sell” recommendations, but the “Under-Valued”, “Best Performing” and “Income” shares should be considered for purchase, while the “Over-Valued” and “Worst Performing” shares can generally be sold to release money for re-investment in more attractive shares.

Brokers Following NTA Equity ity Ratio Yield Ratio

Brokers Following NTA Equity ity Ratio Yield Ratio

OVER-VALUED SHARES: Highest Price/Sales Ratios, Relative Strength < 0

Energy Resource 1101 -4.6 -5.1 64 0-0 1 3.9

STW Comm Group 274 -4.8 -3.7 65 1-0 5 3.9

INSIDER SELLING: Most Insider Selling, Relative Strength < 0

WORST PERFORMING SHARES: Weakest Shares, P/S Ratio > 0.25, Yield < Twice Average

Copyright Securities Research Company Ltd

Australian Warrant / Option Analysis

34 25 1-3 18.0 13.8 +31 0.57 2.03 1.00 +21

14 10 2-10 8.6 8.0 +8 0.66 1.48 1.00 +11

15 20 3-1 4.3 5.3 -20 0.57 1.85 1.00 +17

Diatreme Resources 26 25 1-2 12.0 9.3 +30 0.76 1.98 1.00 +35

Adv Ocular Systems 10 110 1-10 1.5 0.2 +754 0.79 3.13 1.00 +273

Advanced Healthcare 4 12 1-4 0.5 0.0 +999 0.23 9.99 1.00 +160

7 15 1-1 0.2 1.2 -83 0.98 2.23 1.00 +116

Dynasty Metals Aust 23 20 1-6 7.0 10.2 -31 0.83 1.68 1.00 +13

Allco Max Securities 90 100 0-1 0.3 0.0 +999 0.17 9.99 1.00 +999

Eagle Bay Resources 6 15 2-10 3.0 1.1 +162 0.67 2.07 1.00 +52

14 20 0-3 4.0 0.3 +999 0.58 7.53 1.00 +764

13 20 3-1 5.0 0.8 +522 0.21 5.11 1.00 +24

Anitsense Therapeutic 3 20 0-5 0.2 0.0 +999 0.62 7.48 1.00 +999

12 20 1-9 3.0 6.4 -53 1.32 1.38 1.00 +45

147 124 0-0 26.0 0.0 +999 0.40 7.48 1.00 +999

15 30 2-10 5.2 3.4 +51 0.59 2.13 1.00 +35

220 30 1-10 200.0 194.3 +3 0.86 1.12 1.00

Argonaut Resources 12 30 0-10 1.8 0.2 +999 0.57 5.24 1.00 +239

4 20 1-4 0.4 0.1 +511 0.69 3.83 1.00 +239

58 75 0-3 2.3 0.5 +379 0.37 9.99 1.00 +227

12 20 1-4 2.5 0.5 +397 0.37 5.04 1.00 +60

4 32 0-7 0.1 0.0 +999 0.67 9.23 1.00 +999

16 20 0-10 1.1 2.4 -55 0.64 3.03 1.00 +45

156 140 0-9 31.0 31.0 +0 0.35 3.75 1.00 +13

20 20 1-7 6.0 7.5 -20 0.71 1.89 1.00 +18

13 150 1-2 0.2 0.4 -44 1.09 2.81 1.00 +714

Exco Resources NL 27 20 0-0 5.5 0.4 +999 0.72 2.81 1.00 -100

23 20 0-3 6.5 7.9 -18 1.47 2.09 1.00 +76

Fall River Resources 14 25 1-3 4.0 1.0 +315 0.50 3.84 1.00 +79

Australis Mining Corp. 12 20 0-4 2.7 0.0 +999 0.16 1.00 1.00 +577

3 10 2-1 0.7 0.3 +113 0.75 2.36 1.00 +94

5 25 0-4 0.5 0.0 +999 1.15 5.28 1.00 +999

17 30 0-6 6.5 1.5 +333 0.89 3.36 1.00 +361

9 18 0-9 1.0 0.5 +90 0.72 3.65 1.00 +180

7 25 1-4 2.0 0.6 +253 0.87 2.60 1.00 +191

17 20 0-3 2.5 1.7 +45 0.79 4.24 1.00 +207

31 20 0-0 9.5 108.6 -91 0.75 1.17 1.00 -100

40 20 0-10 23.5 21.0 +12 0.58 1.78 1.00 +12

20 25 0-11 8.0 3.9 +107 0.67 2.72 1.00 +73

Global Mining Invest 135 100 0-3 33.5 36.5

6 30 0-10 0.8 0.0 +999 0.77 4.53 1.00 +584

6 20 0-1 0.1 0.0 +999 0.81 1.00 1.00 +999

8 15 0-6 0.5 0.2 +133 0.70 4.85 1.00 +327

3 32 1-7 0.5 0.1 +575 0.96 2.73 1.00 +397

Golden State Petrol. 47 65 0-4 8.0 2.0 +297 0.62 5.59 1.00 +287

Biolayer Corporation 16 35 1-2 3.9 1.6 +151 0.70 2.97 1.00 +114

147 20 1-4 115.0 129.6 -11 1.05 1.12 1.00

7 20 1-0 0.5 0.9 -43 0.94 2.55 1.00 +177

22 20 1-4 6.9 12.2 -44 1.26 1.40 1.00 +18

17 50 0-11 0.9 0.3 +245 0.63 4.64 1.00 +242

27 50 1-3 6.0 1.6 +270 0.49 3.97 1.00 +79

17 22 2-5 7.0 5.5 +28 0.63 1.92 1.00 +26

14 20 0-10 2.5 6.9 -64 1.70 1.45 1.00 +77

4 20 5-8 3.2 0.8 +316 0.57 1.92 1.00 +38

17 20 0-4 2.5 1.1 +122 0.52 5.64 1.00 +132

4 125 4-1 0.2 0.0 +999 0.57 3.47 1.00 +135

43 55 0-2 0.3 0.0 +999 0.27 9.99 1.00 +648

9 20 0-4 0.2 0.0 +999 0.50 9.99 1.00 +999

3 10 0-10 0.4 0.1 +560 0.78 3.97 1.00 +383

18 20 2-4 6.5 7.5 -14 0.74 1.67 1.00 +19

17 20 2-4 9.0 7.8 +15 0.85 1.54 1.00 +27

14 20 3-4 5.0 6.3 -21 0.72 1.57 1.00 +19

32 40 0-8 5.0 11.3 -56 1.30 1.82 1.00 +67

7 25 0-4 0.2 0.0 +999 0.77 8.06 1.00 +999

10 14 0-7 2.5 1.0 +153 0.72 3.52 1.00 +153

20 20 1-7 9.2 7.3 +26 0.73 1.87 1.00 +29

13 15 0-9 4.3 3.4 +26 0.87 2.29 1.00 +69

20 65 1-10 3.4 2.2 +54 0.74 2.48 1.00 +98

18 25 0-7 0.5 2.1 -76 0.71 3.43 1.00 +82

15 20 1-7 7.5 2.4 +216 0.46 3.05 1.00 +47

Hillgrove Resources 23 20 0-4 4.5 4.1 +9 0.50 3.99 1.00 +29

24 20 1-1 8.0 9.0 -11 0.70 2.02 1.00 +15

4 100 0-5 10.0 0.0 +999 0.95 1.00 1.00 +999

4 25 2-4 2.0 0.5 +290 0.88 2.09 1.00 +129

Hunter Hall Global Val107 100 0-8 6.2 11.0 -44 0.11 8.61 1.00

Cape Lambert Iron Ore 42 30 2-2 23.5 21.1 +11 0.61 1.66 1.00 +12

Cardia Technologies 3 10 1-4 0.5 0.2 +109 0.86 2.61 1.00 +177

85 100 1-2 2.4 0.8 +220 0.09 9.99 1.00 +18

47 25 0-0 20.5 0.8 +999 0.48 9.99 1.00 -100

23 20 0-11 8.0 7.8 +3 0.70 2.18 1.00 +24

13 50 0-5 4.0 0.0 +999 0.67 8.85 1.00 +999

13 20 0-10 3.3 0.3 +999 0.37 6.76 1.00 +111

Indigo Pacific Capital 86 150 0-7 1.5 0.2 +645 0.33 9.99 1.00 +164

4 20 1-4 0.6 0.0 +999 0.00 9.99 1.00 +278

Chemgenex Pharm. 51 125 3-7 20.0 8.2 +145 0.48 2.42 1.00 +34

18 20 1-3 4.0 2.4 +66 0.36 3.81 1.00 +29

12 40 1-4 0.3 0.5 -42 0.67 3.39 1.00 +148

16 20 2-1 3.0 7.8 -62 1.01 1.47 1.00 +21

Citrofresh International 18 25 1-9 6.8 5.2 +31 0.75 1.99 1.00 +42

18 20 0-2 2.1 1.9 +9 0.98 4.13 1.00 +305

385 100 0-0 270.0 5.2 +999 0.27 1.99 1.00 -100

17 20 0-5 5.4 2.5 +113 0.79 3.31 1.00 +162

15 20 1-11 4.9 4.7 +3 0.73 1.90 1.00 +33

50 32 0-8 23.0 21.8 +6 0.79 1.95 1.00 +18

16 20 0-9 3.5 2.5 +42 0.68 3.00 1.00 +74

Continental Goldfields 10 20 1-1 2.0 1.8 +11 0.90 2.32 1.00 +107

83 100 0-5 1.3 0.4 +209 0.20 9.99 1.00 +69

12 20 1-9 3.0 1.8 +63 0.55 2.74 1.00 +45

Louisiana Petroleum 10 20 2-8 3.4 2.8 +20 0.69 1.91 1.00 +38

Copyright Securities Research Company Ltd

1 20 3-6 0.2 0.3 -29 1.24 1.46 1.00 +146

Red River Resources 16 20 3-7 7.0 10.0 -30 0.93 1.30 1.00 +16

11 28 1-9 1.7 1.9 -12 0.82 2.16 1.00 +81

147 180 0-6 19.0 0.0 +999 0.00 9.99 1.00 +83

2 10 3-3 0.8 0.2 +246 0.58 2.48 1.00 +61

Malachite Resources 22 20 2-0 8.1 9.5 -14 0.70 1.72 1.00 +14

Regis Resources NL 11 20 5-8 2.6 4.1 -37 0.50 1.72 1.00 +14

8 25 0-3 0.7 0.0 +999 0.59 9.99 1.00 +999

2 40 1-5 0.3 0.0 +999 0.82 4.23 1.00 +752

18 20 0-9 6.0 4.0 +51 0.71 2.65 1.00 +63

2 15 0-5 0.6 0.0 +999 0.82 9.39 1.00 +999

Maximus Resources 15 20 1-10 3.8 3.5 +8 0.56 2.38 1.00 +29

20 20 1-4 8.0 5.4 +47 0.53 2.46 1.00 +29

70 20 0-5 44.0 50.5 -13 0.54 1.39 1.00 -19

Richfield International 22 20 1-3 2.5 7.3 -66 0.60 2.19 1.00

26 25 0-4 4.0 3.3 +20 0.49 4.66 1.00 +47

8 10 0-1 0.5 0.1 +486 0.75 9.99 1.00 +999

18 75 0-4 0.7 0.0 +999 0.52 9.99 1.00 +999

14 26 2-9 1.0 2.3 -57 0.50 2.49 1.00 +29

3 15 0-4 0.2 0.0 +999 0.60 9.99 1.00 +999

20 30 3-3 7.4 10.6 -30 0.92 1.38 1.00 +22

8 25 0-3 0.3 0.0 +653 1.10 5.64 1.00 +999

20 20 1-3 7.0 4.2 +67 0.41 3.11 1.00 +28

Millepde International 4 15 1-6 1.0 0.4 +136 0.83 2.52 1.00 +144

20 20 2-11 8.2 6.8 +21 0.41 2.15 1.00 +13

15 20 1-10 3.5 4.7 -26 0.71 1.96 1.00 +28

19 20 1-7 5.5 8.3 -33 0.88 1.67 1.00 +20

138 115 1-5 50.0 44.3 +13 0.43 2.44 1.00 +13

350 300 0-8 191.0 70.1 +172 0.28 4.16 1.00 +66

Minerals Commodities 20 30 0-10 3.0 2.1 +40 0.62 3.42 1.00 +82

Safety Medical Prod 19 20 2-4 6.5 6.2 +5 0.49 2.12 1.00 +15

5 10 1-10 0.8 0.5 +67 0.55 2.94 1.00 +59

8 30 1-10 1.7 1.1 +53 0.84 2.24 1.00 +112

Saracen Mineral Hold. 37 10 6-10 30.0 31.8

4 10 0-10 0.4 0.0 +999 0.46 7.72 1.00 +269

Saracen Mineral Hold. 37 13 3-3 15.0 27.5 -45 0.59 1.28 1.00

70 100 3-10 18.0 21.9 -18 0.46 2.01 1.00 +15

7 20 1-9 2.1 1.0 +118 0.79 2.32 1.00 +98

7 20 0-5 0.1 0.0 +179 0.79 5.99 1.00 +999

7 30 0-1 0.1 0.0 +999 0.53 9.99 1.00 +999

Murchison Holdings 137 100 2-4 45.0 56.3 -20 0.34 2.13 1.00

Souls Private Equity 19 30 3-4 4.0 1.3 +219 0.22 4.64 1.00 +20

27 20 0-7 13.0 10.8 +20 0.98 1.93 1.00 +46

15 25 2-8 2.7 1.3 +113 0.32 3.73 1.00 +27

8 20 1-4 1.6 0.6 +169 0.64 3.20 1.00 +107

11 20 0-7 2.0 0.6 +259 0.69 4.20 1.00 +228

NGM Resources Ltd 11 20 0-7 2.0 0.6 +259 0.69 4.20 1.00 +228

4 20 0-1 0.1 0.0 +999 0.60 9.99 1.00 +999

Structural Monitoring 13 20 0-8 3.0 0.8 +277 0.60 4.19 1.00 +150

Navigator Resources 23 20 0-10 8.3 6.9 +21 0.66 2.35 1.00 +32

Neptune Marine Serv. 31 20 4-4 12.0 20.5 -41 0.63 1.34 1.00

7 15 2-10 3.9 2.0 +93 0.67 1.92 1.00 +40

New Privateer Hold. 430 115 0-4 55.0 317.6 -83 0.96 1.35 1.00 -94

Northwest Resources 23 20 1-5 11.0 8.8 +25 0.65 1.97 1.00 +23

4 10 0-6 0.5 0.0 +999 0.66 6.03 1.00 +589

14 20 4-1 6.5 7.8 -16 0.84 1.35 1.00 +18

20 100 1-8 4.0 0.4 +997 0.62 3.76 1.00 +169

2 20 1-5 0.2 0.3 -41 1.27 1.96 1.00 +350

Tennant Creek Gold 25 15 0-9 15.0 11.7 +28 0.69 1.91 1.00 +28

16 25 1-4 2.7 1.9 +46 0.54 3.14 1.00 +55

21 30 1-9 12.0 4.5 +165 0.60 2.36 1.00 +51

55 125 2-9 0.5 4.3 -88 0.40 3.33 1.00 +35

11 20 0-7 2.4 0.8 +200 0.84 3.45 1.00 +266

114 100 1-10 12.0 26.6 -55 0.18 3.71 1.00

20 50 1-10 4.0 4.0 +1 0.82 2.08 1.00 +74

2 14 1-6 0.1 0.6 -83 1.67 1.48 1.00 +310

17 20 1-4 3.0 1.8 +65 0.30 4.48 1.00 +25

25 20 2-9 15.0 20.9 -28 1.55 1.10 1.00 +13

10 20 0-4 1.2 0.1 +739 0.79 5.70 1.00 +999

Uranium Exploration 31 20 1-7 13.0 19.2 -32 1.09 1.36 1.00

16 20 0-3 2.0 0.6 +223 0.60 6.43 1.00 +306

18 20 1-10 8.0 6.9 +16 0.74 1.81 1.00 +27

7 20 3-4 3.2 1.1 +189 0.53 2.39 1.00 +42

2 12 1-7 0.4 0.0 +999 0.54 5.43 1.00 +251

Pan Pacific Petroleum 16 15 0-10 5.6 3.1 +81 0.45 3.30 1.00 +41

6 25 1-9 1.3 0.7 +100 0.87 2.32 1.00 +143

8 20 0-4 0.2 0.1 +153 0.90 5.41 1.00 +999

Westralian G & Power 11 25 3-1 3.2 5.3 -39 0.98 1.43 1.00 +36

14 30 1-3 1.5 0.4 +284 0.47 4.65 1.00 +97

19 25 0-10 2.8 2.0 +41 0.51 3.85 1.00 +58

29 20 2-9 17.0 12.7 +34 0.33 2.01 1.00 +10

16 50 1-4 1.5 0.9 +76 0.70 3.24 1.00 +147

50 25 1-0 36.5 28.1 +30 0.69 1.65 1.00 +23

20 20 2-3 5.6 4.2 +32 0.25 3.36 1.00 +12

Zelos Resources NL 17 20 1-4 5.2 5.1 +3 0.77 2.04 1.00 +37

86 20 0-3 68.0 66.3 +3 0.82 1.30 1.00 +10

12 20 0-3 0.5 1.0 -49 1.24 3.42 1.00 +910

Portland Orthopaedics 34 25 2-3 22.0 17.5 +26 0.65 1.61 1.00 +15Prairie Downs Metals 32 25 1-9 15.5 15.7

7 20 0-3 0.1 0.0 +999 0.55 9.99 1.00 +999

Prosperity Resources 9 12 0-9 2.0 1.2 +65 0.64 3.26 1.00 +80Quantum Resources 4 10 5-8 1.0 3.3 -69 1.10 1.15 1.00 +18Quantum Resources 4 10 4-2 1.0 2.8 -64 1.10 1.23 1.00 +25

26 30 0-5 6.1 4.2 +46 0.84 3.10 1.00 +130

Ramelius Resources 19 20 1-4 6.4 5.4 +19 0.64 2.22 1.00 +31

Ramelius Resources 19 18 0-10 6.2 5.1 +23 0.64 2.50 1.00 +35

209 170 0-1 39.0 40.1 -3 0.22 5.2 1.00 +0%

131 100 1-4 35.0 40.8 -14 0.18 3.1 1.00 +2%

79 100 1-4 7.0 4.1 +69 0.22 6.6 1.00 +26%

Copyright Securities Research Company Ltd

Australian Warrant / Option AnalysisAurox Resources (codes AXO and AXOO). Equigold (EQI and EQIO).

Aurox Resources placed 2,000,000 shares at 55 cents in

Equigold has completed the Bankable Feasibility Study

May to raise $1.1 million. These options still have 14

for the Bonikro Gold Project in Ivory Coast and the

months until their final exercise/expiry date and we are

board of directors has approved the development of this

happy to hold to seek further gains.

The capital cost of development will be around

Bounty Industries (codes BNT and BNTO).

US$56 million - plus another US$18 million if the

Bounty Industries has confirmed its forecast of a $5

company buys its own mining fleet rather than using a

million (6.2 cents per share) net profit for the year ended

contract miner. The mine should produce around 785,000

June 2006 - although only $1 million will be from

ounces of gold over a 6¾ year life at a cash cost of

mining and $4 million of profit from the sale of equipment.

US$251/ounce. This will produce a net after tax return

Profits are then forecast to rise to $7 million (7.1 cents

of US$74 million (at an average gold price of US$500)

per share) - all from coal mining - in the year to June

to US$125 million (at a gold price of US$600) for

Those forecasts would appear to justify a significantly

Gold is currently trading around US$645, which

higher value for Bounty Industries shares but there are

would yield an after tax profit around US$150 million.

some inconsistencies. For example, in July the company

The 6¾ year mine can likely be extended by using

placed a further 15,000,000 shares at 20 cents to raise $3

this equipment and plant to mine and process other gold

million to finance future growth. This money will no

doubt help the company expand, but issuing new shares

The company has an indicative offer of an A$50

at only 2.8 times current year forecast profits will not

million loan to partially finance the mine and expects to

increase shareholder wealth. The placement at such a

finalise this financing this month. In addition, the

low valuation suggests that the market - and the directors

company has A$39 million in cash and will receive

- have doubts about the $7 million profit forecast (or that

another A$59 million when the 42 million listed options

earnings per share will be diluted by further low priced

are exercised at $1.40 in May next year. Equigold will

share issues). Raising additional finance at such a low

seek to finalise political risk insurance cover in

valuation dilutes the interests of the existing shareholders

who would do better with slower growth, rather than

Preliminary site work is expected to start in November

effectively selling off part of the company to new

or December, with the main site construction starting in

investors at a P/E ratio of just 2.8.

January 2007. Open pit mining is scheduled to begin in

Our options have just over 4 months until their final

September 2007, plant commissioning in January 2008

exercise/expiry date of 31 December 2006. Each option

and gold production in February 2008.

can be exercised to buy a new share at 20 cents, so the

Equigold options have only nine months (i.e. until 31

market price of the shares needs to appreciate in the near

May 2007) until their final exercise/expiry date at which

future if the options are to have any significant value.

time we have the right to buy shares at 140 cents. Now

Option leverage is a very high 3.84 times, so any

that the company is to develop its Bonikro Gold Project

fluctuation in the share price would have a large impact

the market may re-rate the value of the company's

on the value of the options. “Hold”. Cool or Cosy (codes COS and COSO).

Equigold is a sound gold mining company that will

The company reports a poor second half (to June 2006)

significantly expand its gold production with this project

owing to a mild summer which lowered demand for air-

- so is an attractive investment in this sector.

conditioning, reduced consumer spending and higher

We rate the options a speculative “Buy” owing to

overheads as the company expands its air-conditioning

their short remaining life of only nine months - but they

business nationally. The second half is expected to be

do offer a very high 3.75 times leverage over this period.

“lower than the first half” profits - which was down 75%

- so the annual result could be 70-75% lower at just$430,000 to $520,000 (1.0-1.2 cents per share).

Unfortunately, this company's recent financial

performance has been so poor that the share price hasfallen to a level where it is becoming more likely that theoptions will expire worthless in 21 months. The options- although trading at only 3 cents - are looking overvaluedrelative to the share price. We shall hold our existingoptions in Cool or Cosy but would not recommend newpurchases of options at the current time.

(The shares - on a P/E of 10-12 - could become an

attractive recovery situation if the business improves inthe years ahead, but they would need to recover stronglyover the next 21 months to create value in the options.)

Copyright Securities Research Company Ltd

Financial Resources (codes FRL and FRLO).

the short term but to then sell on-market in July or early

Financial Resources 75% owned subsidiary QuikRent

August to realise the gains on this investment”. IfPty launched its Quikcard, which is a branded VISA card

investors haven't already sold then the best action at

and combined personal loan, in June. All processing and

present may be to exercise the options to buy Image

funding will be provided by Police & Nurses Credit Society with QuikRent marketing the card to national

The are two reasons for this: Firstly, the options

retail groups. By the end of July the company had 28

currently trade at a discount relative to the share price.

groups offering its Quikcard at 1400 sites.

The shares are bid at 46 cents, so the intrinsic value of the

The group's mining contracting subsidiary, FRL

options is 25 cents less or 21 cents - but the options are

Contracting, has won new work at the St. Ives gold

quoted with a bid of only 17 cents. Rather than sell for

mine to construct the Heap Leach Pad Stage 3. Work

17 cents it is better to pay 25 cents to exercise the option

started in July and will continue until early 2007. This

and then sell the shares at 46 cents (plus or minus any

contract will help double the contracting revenues to

fluctuation in the share price) to realise a net 21 cents.

over $20 million for the year to June 2007.

Secondly, Image Resources is planning to spin off a new

We first reviewed Financial Resources in November

company called Magnetic Resources NL, distributing

2004 when the shares were trading at 19 cents and the

these shares to holders of Image Resources shares. This

options traded at 4 cents. Both the shares and options

spin off may add value or help to support the Image

have exactly the same prices today! Three years ago the

Resources share price over the next month or two.

options were very under-valued, but their shorter

Marengo Mining (codes MGO and MGOO).

remaining life (i.e. 21 months until 31 May 2008) means

The company has drilled the first five holes, or about 10-

15% of its current exploration program, at the Yandera

The options still remain attractive for new purchases.

project. Inspection of the first two holes shows they

They offer a very high leverage of 2.79 times and require

“intersected broad zones of mineralisation” at what was

a “break-even rate” of only 14% per annum growth in

previously believed to be the south-east limit of the

the share price before they start to quickly increase in

Gremi Zone. Further drilling will continue to test the

value. Financial Resources is making progress at building

Gremi Zone and nearby Omora Zone which have “good

up its business, so there is good potential for the shares

near surface” mineralisation and “could form the basis

to appreciate in value over the next 21 months.

for a starter pit” mining operation.

Marengo Mining options are fairly valued, offer

reasonable leverage (i.e. 1.67 times) and require a low10% per annum rate of appreciation in the share pricebefore an investment will “break-even” and then start toincrease in value. There is still 18 months until the finalexercise/expiry date - so if Marengo Mining can advanceits exploration over that period then the shares (and theoptions) could be re-rated strongly. “Buy”. Metroland Australia (codes MTD and MTDO). The company has entered a conditional contract to refurbish its building at 16-20 Mountain Road, Ultimo, into offices and sell it for $19 million. The building was Global Mining Investments (codes GMI and GMIO).

purchased in June 2005 for $8.45 million and refurbishing

These options reach their final exercise/expiry date in a

little over three months - on 30 November 2006. At that

The September 2005 contract for the sale of the

time we will have the right to buy a share at 100 cents.

Neutral Bay Property was settled on 7 July for $12.2

Global Mining Investments shares currently trade

around 135 cents (and have a fully diluted net asset value

The company has also entered a conditional contract

of 141 cents) which gives the options an intrinsic value

to purchase the properties at 218-240 Queen Street,

of 35 cents. Investors can either (1) exercise the options

Campbelltown for $14.8 million (plus GST). The

and remain an investor in the shares or (2) sell the

property on a 6,579m2 site has 24 tenants and a current

options on-market to realise their value.

gross rental income of $1,224,000. The local council is

Global Mining Investments is a suitable investment

encouraging the regeneration of the area and Metroland

for investors wishing to maintain an exposure to global

sees “significant scope to improve the current income”

mining shares - so exercising the options is an attractive

and “intends to extensively redevelop the property”.

choice in this situation. Of course, investors who do not

We first reviewed Metroland Australia in February

have sufficient cash to exercise all of their options - or

2005 but since then the shares have fallen 36% to 14

who would find themselves over-exposed to this company

cents and the more volatile options are down 78% to 1

or sector - should look to realise some of their options

cent. At this price, however, the options still offer an

on-market over the next few months (or sell off some of

attractive - albeit high risk/high return - speculative

the shares after exercising the options).

investment. So higher risk investors could consider asmall dollar investment in the options, if they are

Image Resources (code IMA and IMAO).

available. Unfortunately, at current prices the options

Our recommendation in May was to “hold the options in

are inactively traded. (Continued on Page 12)

Copyright Securities Research Company Ltd

Warrant/Options (Continued from Page 11)Stirling Products (codes STI and STIO). ORT (codes ORT and ORTO).

Cash short Stirling Products has raised $2.3 million

ORT holds $1.6 million in cash - or about 1.07 cents per

from two placements totalling 20.0 million shares at

share. These options still have 18 months until their

11½ cents (plus 10.0 million options to buy shares at 20

final exercise/expiry date - but are unlikely to have any

Stirling Products has signed the contract formalising

the Heads of Agreement announced in December 2005

Orchid Capital (codes ORC and ORCO).

with South African based Afgri. Afgri will fully fund

Orchid Capital's 23.2% owned Jiva Kata Resort

studies on poultry, swine, sheep and cattle required to

Company has sold its hotel property in Phuket, Thailand.

obtain registration and commercialisation of

Orchid Capital's share of the first instalment was ThB

R-salbutamol in South Africa. Stirling Products will

17,632,000 (A$608,000) and up to another ThB

own the production registrations and trade marks,

23,200,000 (A$800,000) over the next 16 months, subject

appointing Afgri as its sole agent in South Africa for up

to conditions relating to enlarging the hotel. This will

realise a significant gain over the investment's book

Stirling Products joint venture with Equine HealthCare of Denmark will incorporate a joint venture

Orchid Capital is continuing to focus upon its new

company, Pulmovet ApS, which will then raise

strategy of investing in small Asian companies which

additional capital in Europe to fund trials for the

hope to list on stock exchanges over the next few years.

registration of its treatment in Europe and the United

Net asset backing per share is 2.95 cents.

States for heaves in horses. The treatment uses a device

Our remaining Orchid Capital options will probably

invented by Equine HealthCare and Stirling Products'

expire worthless on 30 November 2006. Fortunately we

previously sold around two-thirds for a significant

Unfortunately the share price has fallen so much that

it would now need to appreciate 107% per annum over

the next 16 months for the options to have any value. That is not impossible - as this is a very volatile situationand the Stirling Products share price could appreciatevery strongly - but is not likely. We shall continue tohold our Stirling Products options but realistically weshould expect that they will expire worthless, so wewould not make new purchases at this time. Total Return Index for All Listed Shares

The next issue of Market Analysis will be emailed in five

weeks time on Monday September 11, 2006.

The print version will be delivered later that week,

depending upon printing and postal delivery times.

MARKET ANALYSIS is published 12 times per year by Securities Research Company Limited, P.O. Box 34-162, Birkenhead, Auckland. Subscribe online at www.stockmarket.co.nz or www.australia-stockmarket.com or email [email protected]. Readers are advised that they should not assume that every recommendation made in the future will be profitable or equal the performance ofrecommendations made in the past. A summary of All prior recommendations is available is published on the website. The information presentedhas been obtained from original and published sources believed to be reliable, but its accuracy cannot be guaranteed. The entire contents are copyright. Reproduction in whole or part is strictly forbidden without the approval of the publisher.

Copyright Securities Research Company Ltd

Pediatric Neurology Weill Cornell Medical Center Barry Kosofsky, MD New York Presbyterian Hospital Chief, Pediatric Neurology 505 E 70th Street 3rd Floor Zuhal Ergonul, MD, PhD PEDIATRIC HEADACHE QUESTIONNAIRE Please complete this questionnaire. It will be an important part of your child’s medical record. How did you learn about our practice? Pediatrician :

Sonstige Marktregeln Gas Kapitel 2 Teil I - Beziehungen zwischen den Marktteilnehmern Teil II - Informationsübermittlung von Netzbetreibern an andere Marktteilnehmer für die Marktgebiete Tirol und Vorarlberg Beziehungen zwischen den Marktteilnehmern Das vorliegende Dokument soll einen Überblick über die Beziehungen und den not-wendigen Datenaustausch (Fahrplän

Twenty Five Years of Independent Information and Unbiased Advice on the Australian and NZ StockmarketsMarketAnalysis

Circadian Technologies realises significant gain . 5

Cellnet Group's financial position improves,

Summary and Recommended Investment Strategy.

Twenty Five Years of Independent Information and Unbiased Advice on the Australian and NZ StockmarketsMarketAnalysis

Circadian Technologies realises significant gain . 5

Cellnet Group's financial position improves,

Summary and Recommended Investment Strategy.

Recommended Investments (Cont'd from Page 3)

services can vary significantly on a month to month

Renaissance Corporation sees its competitive

Campbell Brothers has increased its holding in CCI

Recommended Investments (Cont'd from Page 3)

services can vary significantly on a month to month

Renaissance Corporation sees its competitive

Campbell Brothers has increased its holding in CCI Centennial Coal has downgraded its profit forecast

Centennial Coal has downgraded its profit forecast Australian Warrant / Option Analysis

Aurox Resources (codes AXO and AXOO).

Australian Warrant / Option Analysis

Aurox Resources (codes AXO and AXOO). Financial Resources (codes FRL and FRLO).

Financial Resources (codes FRL and FRLO). Warrant/Options (Continued from Page 11)

Stirling Products (codes STI and STIO).

Warrant/Options (Continued from Page 11)

Stirling Products (codes STI and STIO).